Probability Updated. Old Version Archived. Running New Version.

Concentration works when your prior is built on information saturation; without it, "holding forever" is just sunk cost in a good suit.

Quick update for paid members: If there’s a company you’d like me to analyze, feel free to DM or email me. I’ll prepare the report and add tracking tools for you to monitor key updates and news. The goal is to turn 30 days of information into a concise summary of the insights that matter most — saving you time while keeping you informed. As long as your info you configure to the tracking apps is very high-quality and low-time decay, it will deliver high-quality conclusion or signal.

1. What a Belief Actually Is

I am a Bayesian belief holder.

You believe something. “It will rain tomorrow.” That belief is not scripture. Not a nail in bone. It is a number: 65%.

This is what a belief looks like to a Bayesian. Not yes or no. Not right or wrong. A probability distribution — a temporary number with the door always open to revision.

Every judgment you make — will this stock rise, is this job right for me, can this person be trusted — is a set of numbers running quietly in the background of your cognition.

Most people do not see their beliefs this way. They treat beliefs as property. As organs. Something to defend, because losing one means losing shape.

That is the source of most avoidable suffering. It is also the mechanism behind the Bayesian’s edge.

2. What Updating Actually Does

The world sends signals continuously. Some are clear (”thunder outside”). Some are ambiguous (”my boss didn’t reply today”).

Before any signal arrives, you already hold a prior probability — a starting point built from accumulated experience and knowledge.

Then a signal arrives. Bayes’ theorem does one thing, without sentiment: it takes the information content of that signal and folds it into the before produce a posterior probability.

That posterior is what you should believe right now, given all available information. It simultaneously becomes the prior for the next signal. The process has no terminus, no final truth — only continuous approximation.

In this model, updating is not betrayal. Updating is how the system runs. Refusing to update is not loyalty to principle. It is loyalty to a past version of yourself, dressed up as thinking.

3. Why Loyalty to the Old Self Is Seductive

It offers cheap continuity. The brain is deeply averse to fragmentation.

If I repudiate yesterday’s judgment, will I repudiate today’s tomorrow? If I keep negating, am I still “me”?

This fear pins people to outdated positions. They build rhetorical scaffolding to keep the old conclusion standing past its expiration.

In investing, this is called “your position determines your view.” In daily life, “dying to save face.” In cognitive science, “confirmation bias” and “sunk cost fallacy”

The shared formula: prioritize “was I right?” over “did I accurately read reality?”

The Bayesian breaks this formula by redefining identity. He is not the statue fixed at a conclusion. He is the algorithm itself — the continuous probability updating process. The output changes constantly. The algorithm’s identity holds. Water flows. Riverbed stays.

The critical operation: can you separate self from opinion? Can you recognize that your view is rented accommodation, not ancestral property? Your judgment is a hand of cards — play it, lose, draw again. You are not putting your identity on the table.

4. What This Looks Like in Practice

The late delivery. Food arrives 40 minutes late. Emotions accumulate. The rider appears — sweating, apologizing. Does that signal update the belief “this restaurant is unreliable”? Then you open the box. Cold food. Two signals, both real, both need processing simultaneously. A calibrated Bayesian assigns the bad review to the cold food. Not to the rider. Blame apportioned to evidence.

The silent friend. Two weeks, no contact. Prior: “We have a good relationship; he reaches out.” Signal: silence. The brain auto-generates explanations, each with a probability. How much weight goes to “he dislikes me now”? That weight depends on your self-model, the relational history, and your base rate for human behavior. The trained Bayesian does not sprint to the most painful explanation. He does not self-soothe with “he’s just busy.” He carries the open probability distribution forward, waits for the next signal, and says explicitly: “I don’t know the answer right now. This is uncomfortable. I can tolerate it.”

The declining industry. Five years in. Signals: fewer positions, stagnant pay, structural technological disruption. The prior was “I chose the right track.” The threat is not to a single belief but to an entire career narrative. Most people’s response is denial: “It’s a temporary cycle, real value will come back.” They grip the prior not because it remains credible, but because updating the posterior costs too much. The Bayesian sits down and assigns a serious probability to “permanent industry decline.” He sets thresholds: above 40%, start interviewing; above 60%, hard switch. The pain is still there. He converts it into action rather than emotion.

The investment position. Initial judgment: management is solid, sector has growth, prior says “worth high conviction.” But built on what? A handful of research notes, one or two earnings calls, and fragmented news. The information set is sparse, lagged, and updates far more slowly than the market.

I add two things.

First, an AI Agent that scrapes financial statements, industry call transcripts, supply chain filings, regulatory documents, and generates a structured analysis — not a “buy” or “sell” conclusion, but a decomposed probability map: confidence intervals on execution quality, scenario branches for downstream demand, current weights on key risk factors. It does not make the decision. It produces a denser, more systematic prior.

Second, I will build a monitoring tool for you guys. It does one thing: continuously scan for 30 days’ signals tied to this company — semantic drift in customer reviews, skill pivots in hiring patterns, timing lag between raw material cost shifts and gross margin impact — and surface them in real time. Each signal is a micro-update event. No need to redo deep research every day. Act when signals accumulate past the threshold that materially shifts the distribution.

Together, these two tools resolve a structural tension: investment decisions require high-quality information fusion, but human bandwidth for information processing is severely constrained. Previously, this gap was bridged by “experience” and “intuition” — opaque, unverifiable cognitive shortcuts substituting for systematic probability updating. The AI report raises prior precision by an order of magnitude. The monitoring tool compresses the signal-to-update latency from days to hours.

Does this mean AI should trade directly? No. AI accelerates and densifies the Bayesian update cycle. It cannot replace it. A model can read ten years of financials in sixty seconds and output probabilities — but it does not know which probabilities belong in your utility function, how much drawdown you can absorb today, or what failure on this position means to you. Your capital property determines your strategy. Those are the self’s domain.

Bayesianism never said, “let the machine update for you.” It says: use every available tool to approximate the optimal posterior, then keep the decision responsibility.

The appropriate role for AI in investment is not a trader issuing orders. It is an untiring information processing layer — compressing noisy reality into structured probability signals, handing them to you as the final Bayesian updater. Your only remaining task: receive, update honestly, and act.

5. The Buffett Reconciliation

Buffett’s philosophy in one sentence: find a small number of businesses you genuinely understand, buy at a reasonable price, concentrate, hold — rarely sell. Research is front-loaded. High conviction, then active noise-filtering. Frequent updating is a flaw, not a virtue. “Our favorite holding period is forever.”

This appears to directly invert Bayesianism. Bayesianism says beliefs must update continuously on new signals. Buffett says beliefs must be robust enough to survive all noise. One is fluid. One is anchored. One treats updating as the system’s operating mode. One treats not updating as proof of discipline.

Is the contradiction real?

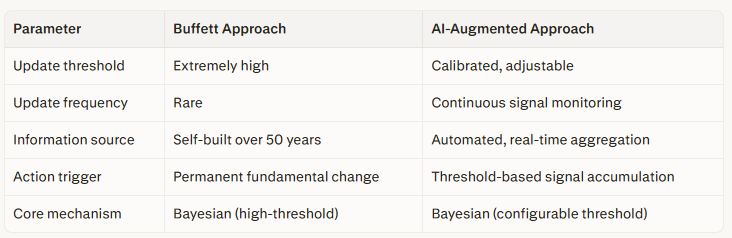

Look more carefully. Buffett does not reject Bayesian updating. He sets the update threshold extremely high. He receives signals. He requires them to be extremely strong and extremely rare before they trigger a revision. His prior — “this business will generate superior returns over the next twenty years” — is built on extraordinary information density. His noise filter is correspondingly severe: quarterly earnings variance is not a signal; macro forecasts are not a signal; a 50% price decline is not a signal. Only permanent, irreversible fundamental change — management credibility destroyed, moat eliminated by technology, capital allocation logic collapsed — triggers an update.

This is high-threshold Bayesianism. It is not in opposition to low-threshold, high-frequency updating via AI Agent and monitoring tools. There are two parameter configurations:

Which is superior? It depends on your information quality and your calibration accuracy.

Buffett runs the high-threshold strategy on a self-built information infrastructure: hundreds of annual reports per year, direct management access, five decades of accumulated pattern recognition across insurance, consumer, and financial sectors. He is not “refusing information.” He is selecting only for signals that exceed an extremely high quality bar, built from information saturation. The concentration is not laziness. It is subtraction from redundancy.

The average investor — or the fund manager spread across too many sectors — who runs “hold forever” is almost certainly not practicing discipline. He is furnishing his confirmation bias and sunk cost fallacy with a respectable-looking coat. He lacks Buffett’s database, information quality, and prior precision. In that context, “not updating” is not wisdom. It is arrogance.

AI Agent reports and monitoring tools close this information quality gap. They let you build priors with substantially higher precision than was previously possible, while detecting truly update-worthy signals substantially faster. You do not become a high-frequency trader because you use AI. You still set your own thresholds. You still run concentrated, long-horizon positions. But you are no longer crossing noise on faith. You are making the “hold” decision through an auditable probability system.

The same outcome — not selling — but one is a bet and the other is a calculation.

The real distinction between the Bayesian and the Buffett-style concentrator is not “update vs. don’t update.” It is one honest question: is my threshold calibrated to my actual information advantage and cognitive capacity, or is it calibrated to my fear of self-negation?

Bayesianism is the operating system. Concentration is an application. The OS manages signal intake, weight assignment, and threshold configuration. The application is the specific strategy you run under those parameters. You can run “high-threshold, concentrated” today and “reduce, diversify” tomorrow as new data arrives. Application changes. OS does not. The self — the continuous updating algorithm — remains intact.

But strategy must also match the nature of your capital. Hard-earned capital that supports your family and your children cannot be treated like speculative capital. The responsibility of the capital determines the level of risk you can take.

6. The Actual Trait

The Bayesian’s shared characteristic across all these scenarios is not calmness. Not rationality. It is something deeper: willingness to let reality serve as the ultimate source of information, and willingness to pay the cost of revising the self in response.

This is not a technique. It is a personality structure. Self-fluidity.

A fluid self is not without principles. Its principle is precisely that all principles are best-current-approximations, revocable by better information. A higher-order principle with fallibility at its core.

In capital markets, the most expensive asset is not gold or oil. It is this fluidity. A fund manager who updates quickly — his maximum drawdown rarely comes from the market. It comes from his self-correction speed. He cuts losses faster not because he feels less pain, but because he has redefined “acknowledging error” as part of the profit function rather than the loss function. He drives the cost of self-updating below the market average.

In life: the people who expand rather than contract over time are not always correct. They say “I was wrong” with the same frequency as breathing. They do not spend two hours disputing a fact. They receive evidence and say, within five seconds: “Oh, I had that wrong.” Then the conversation moves forward instead of catching on the point of who was right.

7. The Time Philosophy

Bayesianism is fundamentally a philosophy of time.

It acknowledges time’s unidirectionality and the world’s irreducible unpredictability — then gives you a methodology for continuously rebuilding the self inside that flow. You do not stand outside time pretending nothing has changed. You move with it, letting each new moment update you.

Yesterday’s judgment was the best available judgment given yesterday’s information. It completed its function. Today, new signals arrive. A new version is required. This is not betrayal. It is growth.

The next time you find yourself defending an old position hard — stop. Ask one question: am I protecting the truth, or am I protecting the version of myself that once believed something?

If it is the latter — that version has retired.

Open the cognitive terminal. Type the command:

Probability updated. Old version archived. Running new version.

The Bayesian’s practice — not defeating the market, not defeating other people, but burying the rigid, heavy, change-averse old self in each yesterday. Then, each morning, receiving the world’s signals again, as if nothing has been pre-committed.