Take-Two Interactive Software, Inc. (NASDAQ: TTWO)--Deep Value Investment Analysis

The GTA VI binary is real — but the floor shifted, and that changes the risk math in a specific, trackable way.

Published: May 14, 2026 | Price: ~$224.89 | Market Cap: ~$41.6B

Fiscal Year End: March 31 | Sector: Interactive Entertainment / AAA Video Game Publishing

Most Recent Confirmed Data: Q3 FY2026 (December 31, 2025)

⚠️ This note is provisional pending Q4 FY2026 actuals on May 21, 2026

Sector Classification Note

Take-Two is not a software company in the SaaS or enterprise sense. It is a AAA video game publisher with a hybrid revenue model: premium game sales (title launches), recurrent consumer spending (live services, in-game transactions, virtual currency), and a mobile-casual segment inherited from the Zynga acquisition (2022). Standard software metrics — ARR, NRR, CAC/LTV ratios — do not apply. The relevant metrics are Net Bookings, Recurrent Consumer Spending (RCS), and pipeline value.

Section 1: Business Model

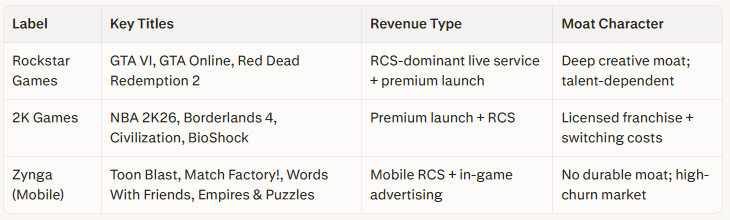

Take-Two operates through three publishing labels with distinct revenue profiles, moat characteristics, and risk exposures.

Revenue Model — Three Streams:

Premium launch revenue: Recognized at point of sale; highly lumpy and title-event dependent. Drives large quarter-to-quarter variance.

Recurrent Consumer Spending (RCS): Ongoing monetization from live service engagement — virtual currency, in-game purchases, DLC, subscription (GTA+). RCS accounted for 80% of total Net Bookings in FY2025 and has been growing. This is the highest-quality revenue line: recurring, high-margin, and relatively immune to release cycle volatility.

Mobile advertising: A third stream via Zynga. After a significant deterioration (advertising revenue fell from $517M to $357M in comparable periods through FY2025), this line reversed in Q3 FY2026, growing 10% YoY, driven by higher average revenue per daily active user. Trajectory is now stabilizing.

Customer Profile: Global consumers across PC, console (PS5, Xbox Series X), and mobile (iOS, Android). No meaningful B2B revenue. Revenue is platform-dependent — PlayStation, Xbox, Nintendo, Apple App Store, and Google Play all extract 15–30% platform fees, representing a structural gross margin ceiling that cannot be negotiated away.

Key Upstream Relationships: Human talent is the critical supplier. Platform holders (Sony, Microsoft, Apple, Google) are mandatory distribution intermediaries with significant fee power. Development costs are capitalized as software development costs on the balance sheet — a major accounting and risk consideration addressed in Section 2.